Betterment Cranks up Features and Costs – is it Still Worthwhile?

From my 2015 visit to check out Betterment's operations in NYC (photo: museumhack)

Since 2014, I've been using the Betterment investing service for a growing portion of my own savings. I funded an experimental account with $100,000, and have had a monthly auto-deposit adding in an additional $1000 per month since then. The results have been documented on a page I call The Betterment Experiment.

So far, the experience has been better than I had expected. The company's behavior - both to me as a customer, and through their relationship with the public and the media has been solid and classy. And their already-good investment system has continued to advance. I joined for the automatic rebalancing of shares, but since then have been impressed by two more obscure features that are surprisingly effective:

- The tax loss harvesting system, which has sliced several thousand dollars from my income tax bill so far. (Note - this feature is generally most useful only at higher income levels, and I got extra benefit from having other capital gains to offset)

- Tax Coordinated Portfolio Allocation, which automatically shields more your of dividend-paying index funds in your IRA instead of your taxable account. I just enabled this last month and am enjoying watching the results.

For people actually saving for retirement, there's also stuff like an impressive retirement guide system and customized advice, but these are less useful to me personally. Because this blog's readership includes many technical and DIY-everything people, I wanted the Betterment account to stand on its numbers alone, not just feelgood convenience features.

I calculated that the tax-related features were easily increasing my return by over 1% per year, which easily covered Betterment's 0.15% annual management fee. I still see many criticisms* popping up around the internet, accusing me of being a "shill" for Betterment and that everyone should just manually run a Three Fund Portfolio in Vanguard. But so far none of them have correctly accounted for these tax savings in their calculations - they underestimated TLH. It's an easy oversight to make without holding a Betterment account yourself and watching the results.

As my positive feelings about the company grew, I continued to move more personal investments over to a second, private account at Betterment, including my old work IRA. As a result I now have about $500,000 with Betterment.

Logically, this was still only a partial commitment - the numbers worked out in favor of sending all my future investment dollars to Betterment, but I was still building trust in the company, so I decided to take it slowly. On top of that, my older investments (mostly with Vanguard), have gone way up in value since I made them in the early 2000s, so it would be tax-inefficient to sell them just to buy similar index funds through Betterment.

Then, They Dropped This Bomb

(Update: after writing this post, I had the opportunity to exchange several private emails with Betterment founder Jon Stein and other employees, and they were quite reassuring. He also posted a much better explanation of why they changed prices, here. So I have updated this section to reflect what I learned.)

On January 30th, I got a preliminary note from the company announcing that their fee structure was about to change. The original tiered price structure looked like this:

- 0.35% on the accounts under $10,000 (with auto-deposit)

- 0.25% on accounts $10,000 to $99,999

- 0.15% on accounts over $100,000

They announced an upcoming change to a flat fee, with a cap

- 0.25% on all accounts up to $2 million

- Free management on the portion of your balance which exceeds $2 million

In other words, your fee is capped at $5,000 per year.

They also added personal consultation services called Betterment Plus and Betterment Premium for higher rates, and I have heard these are welcome services for many customers. But since I greatly prefer talking to computers rather than people when it comes to the subject of money, we're focusing on the robo-advisor service - now called Betterment Digital - here.

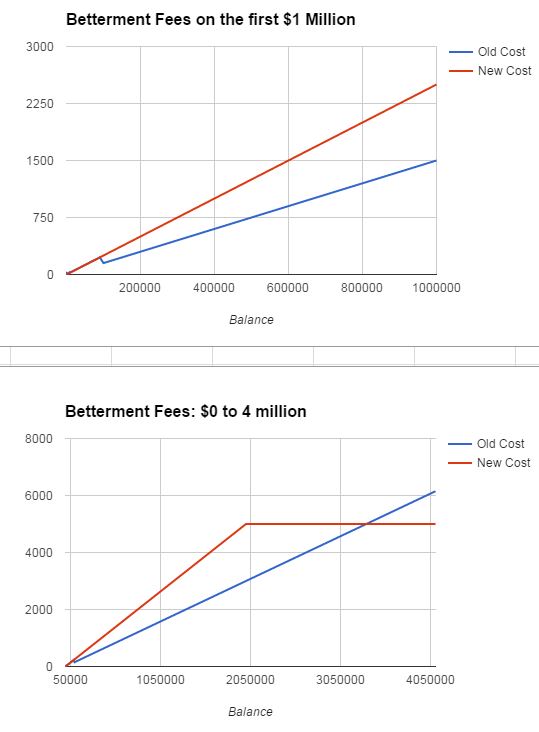

In practice, the two fee levels look like this. The first graph shows what happens on balances up to $1 million, while the second graph is just a zoomed out version showing up to $4 million. The new fee structure will cost significantly more for the wealthier readers of this blog - it only starts to save you money at around $3.3 million in investments.

People with under $100,000 in their account will notice no difference. Those of us in the $100k-$2 million band will see a 66% increase in fees (starting on June 1st), then things even back out by $3.3 million.

In my situation (a $500,000 balance), the annual management fees jump from $750 to $1250 per year, an increase of $500.

How do I feel About This?

These days, I try to avoid outrage and instead think about the big picture. The price change brought up some questions:

- Why is the company increasing fees? Are they correcting a past mistake, having realized it's hard to make a profit on 0.15%? Are they being opportunistic? Are they plumping up the company in preparation for sale?

- Is the service still a good value at for me 0.25%?

- Is there a risk that this will happen again? Investing large chunks of your life savings requires a huge amount of trust. In my opinion, this sudden price change was a violation of my trust - it sets a precedent and I wondered if it could happen at any time. Sure, you can always pull your money out at any time, but this is a hassle with potential tax consequences. Good investors leave money in place for decades and don't want to be forced to move it around.

Question #1 is a philosophical one. I am rooting for Betterment and I like the people who work there. In general, I try to do business exclusively with companies that pass this test. And this makes me less of a customer and more of a partner. I want my business partners to make money off of their customers, including me, because that's what will keep them in business. Being a customer should never be an adversarial relationship.

After talking to Jon, I learned that the price increase was a necessary thing to remain a growing and sustainable business. Doing the math, they manage $6 billion, and at 0.15% they would only collect $9 million in annual income. Far too little to go around in a firm with 100 employees. Sure, they are winning new customers quickly, but that is a very slim margin at this stage. Jon said he would prefer to drop prices as the company grows large enough to allow it, but first we have to get there. He also said their goal is to become an independent, public company.

Question #2 is just a math question, and the answer is Yes. It is overwhelmingly clear that my Betterment account delivers more than 0.25% net annual improvement over trying to manually approximate its performance with Vanguard ETFs. Their software is incredibly good, and just keeps getting better. The talent level of the people there is insane**.

Question #3 was the real stumper for me. This price increase came out of nowhere, and nobody asked me for my opinion - as a customer or as a long-time promoter who has sent thousands of other customers to Betterment. When I got the short advance warning, I spent the day emailing with the marketing department and even the founder, trying to talk them out of it, because I feel that it was placing the trust of customers at an incredible risk. From my email to their team:

" the single biggest weakness that Betterment has (which it is gradually overcoming), is trust ["]When you raise prices on existing customers (and even on future customers in the middle of the customer acquisition stage) this trust is partially or completely shattered.

Investing millions of dollars over a lifetime requires a much more stable policy that reassures people over a period of multiple decades. The good news is that the profits are still there - one wealthy person may have the investments of one hundred or even one thousand beginner investors. But Betterment is still a brand-new company working on acquiring its first foothold of trust for larger, more conservative investors. Is this worth it?"

This is a human behavioral finance problem straight out of a textbook. As humans, we are subject to the cognitive bias called "Loss Aversion" - we fear and perceive the loss of what we currently have much more than we fear and perceive missed opportunities for much larger amounts of gain.

For example, which of the following two options would you prefer?

- an anonymous vandal does $1000 of damage to your car in the parking lot at work, or

- you car-commute uneventfully to work for a few months - but unknowingly miss the opportunity to ride your bike, which would improve your financial picture by much more than $1000?

Complaints on my Twitter feed about Betterment price change - click for larger

That second option should be much more scary to every office worker, but it's not. And yet Betterment has walked itself right into the same trap - subjecting the wealthier portion of its 200,000+ customers to loss aversion.

(Related Reading: here's an earlier article about one of my favorite books of all times, called Predictably Irrational - it teaches you about more of your own flaws in a very entertaining way.)

I feel that a much better business move for Betterment would have been to spend less money on developing new features, in order to be able to leave the existing price structure in place.

But given the current path, I now think the biggest problem was the way they communicated the price change. It was mentioned in passing as part of a cheerful "Look what's new at Betterment!" email to customers. It's the communication style we have come to expect from Verizon or Comcast, but not from a place as genuine and authentic as Betterment.

You could see the pain in the passionate essays that customers immediately sent to my email inbox this week, and in the responses to something I put on Twitter. One guy even started a petition on change.org in an attempt to communicate customer dissatisfaction.

The net result for me will probably be no change. I'll leave the Betterment Experiment running, and continue to deposit the $1000 per month, because that's exactly what an experiment is for - I leave it running so we all get to watch the long-term results.

I still plan to transfer more into my private account over the next year, but I will make a point of reviewing the other robo-advisers and competing services from Wealthfront, Schwab, Vanguard, and WiseBanyan in order for this blog to be less Betterment-specific. My trust was shaken and then mostly reassured in this case, but I don't want readers in this blog to follow in my footsteps without considering all the options independently.

An investment company making management fee increase is a very small deal in the grand scheme of things. But it is a big deal to me because I really try to keep my recommendations useful.

-

* To these critics I say "I respect your hardcore Vanguard chops but please try to separate Bogleheads ideology (which holds that anything not Vanguard is automatically Evil) from the actual numbers. Beating the market is not a viable goal, but reducing account-holder mistakes and reducing taxes is much riper area to harvest. Betterment only has to accomplish this at an 0.25% annual rate to justify their fee.

** Observe this white paper they published explaining the details of new Tax Coordinated portfolio. They just operate on a higher technical plane than other companies.

Disclosure: Betterment's real relationship to MMM - After I invested with them in 2014, I also joined their affiliate program as I do with any product I use and like (see my Affiliate policy). Then I got kicked out, because more recent SEC rules state that you cannot be an affiliate while also having a "testimonial" review. I felt a review is useless if you can't report on your own experience, so I decided to leave the program so I could leave my review up. No problem, of course - my goal is to never let affiliation affect my recommendations as there is plenty of money in life either way. Later, Betterment paid to have flat-rate advertising on this site, and that program may or may not continue - this article might make me a less desirable advertising platform, and I didn't check with anyone before publishing it.