Early Retirement is an Impossible Dream for Most

We're about four years into this blog, and at this point I finally have to admit I am a complete and total fraud.

We're about four years into this blog, and at this point I finally have to admit I am a complete and total fraud.

I mean sure, I saved enough to retire in just nine years and have had a great time running around like a free man in this subsequent decade. But that was an isolated incident, which is a useless model for the average American. Above-average incomes, an appreciating market for stocks and houses, an unusually cooperative girlfriend-turned-wife, and of course plenty of White Person Privilege* came into the picture. It was really luck and fate that got us here, rather than individual effort and choices.

Just look at the bleak picture that the average person faces today in comparison. A dying economy**. Stagnant wages since the 1970s. Sky-high healthcare costs that just keep on rising. Long, congested commutes that could become unaffordable overnight on the whim of any Saudi oil minister. Poor school systems that necessitate private school if you want to live anywhere even close to affordable. A massive load of student loan debt from the ever-increasing cost of university tuition. The list goes on and on.

If you need proof to go with all those negative statements, just look at the results. Americans are facing a retirement income crisis, with far too little in the average senior's 401(k) plan to maintain their current standard of living, even when combined with expected payouts from Social Security. With budgets already stretched razor-thin, it is impossible to expect the average person to cut any further - either before, or after retirement. Did you get the memo? 73 is the new retirement age. Sorry, but that's the way it is, nothing you can do about it.

The great experiment of the personal 401(k) plan, foisted upon us by the elites since the late 1980s is a proven failure. The government and our employers should be providing for our retirement through guaranteed lifetime pensions, rather than forcing us to navigate the murky waters of personal finance alone. I feel I have misled you these past four years, functioning only as a pernicious savings scold and encouraging pointless individual effort, when instead we could have focused our collective efforts on reforming our system.

Oh, and April Fools, of course.

I sure hope you didn't believe those are really the views of Mr. Money Mustache.

Although I did my best to make the awful shit in those preceding paragraphs sound pretty mainstream, it was extremely painful to type it into my computer. My keyboard started to shoot sparks out of its orifices and it is now oozing pus and blood onto my desk. Thoughts like those are so pointless, self-defeating, and just plain wrong and it amazes me that people keep cranking them out.

The problem is not with the intentions of my detractors. These are public-spirited people who are genuinely trying to improve the world. Our difference of opinion lies only in which method we use to get the job done.

The writers who harp about "America's Retirement Crisis" are really attempting to get the politicians to do something about it: increasing funding to the Social security system and throwing a leash on the some of the nastier elements of the financial industry, who set people up with high-fee 401k plans and then sit back and skim their profits for life. These are fine goals, as long as any rules are implemented in an open and scientific manner, without resorting to rhetoric and fear in the political battle to get them implemented. But as you have noticed, I prefer a different approach.

See, the problem occurs when you rob an individual of the belief that he is in control of his own situation. When you spread the social meme that the the system is stacked against us, and that the system needs to change in order to improve our lives. Whether or not the accusations contain a degree of truth does not matter - you train a legion of powerless people who can't take care of themselves, you also end up with lazy voters who are easily manipulated by whichever politician will stoop the lowest to appeal to their cheapest emotions.

Just look at the excuses that go around unchallenged these days. We whine that the national savings rate is only 5% and that the average person in their 60s has only about $100,000 saved. But then nobody mentions that only one percent of trips are made on bicycle in this country, and the majority of travel and commuting is done in single-occupant vehicles bought with dealer financing.

We talk about healthcare expenses as if they are imposed upon us, despite the fact that most of the nation's health spending is done to treat self-imposed diseases related to the biggest four factors: exercise, diet, stress and sleep. US residents spend over $20 billion dollars on soft drinks - a beverage so evil and toxic due to its sugar concentration that any figure above zero is astounding to me. The shit shouldn't even exist, and yet we guzzle it by the tankerload! You can't prevent the truly random and unpreventable, but you can lower your expected lifetime cost drastically.

How could anyone possibly complain about having money problems, while simultaneously paying tens or hundreds of dollars per month to have passive video entertainment and commercials streamed into their house? People are simultaneously robbing themselves of money and the necessary mental quiet time that is a prerequisite to getting ahead - building skills, meeting people, getting better jobs or starting better businesses.

The average person spends over 95% of what they earn and burns most of it on necessities that aren't really necessary. We borrow money and drown in the interest payments. We spend most of our energy working directly against our own best interests. Somebody needs to call bullshit on this practice, because we're not going to fix it just by raising everybody's allowance in their retirement years.

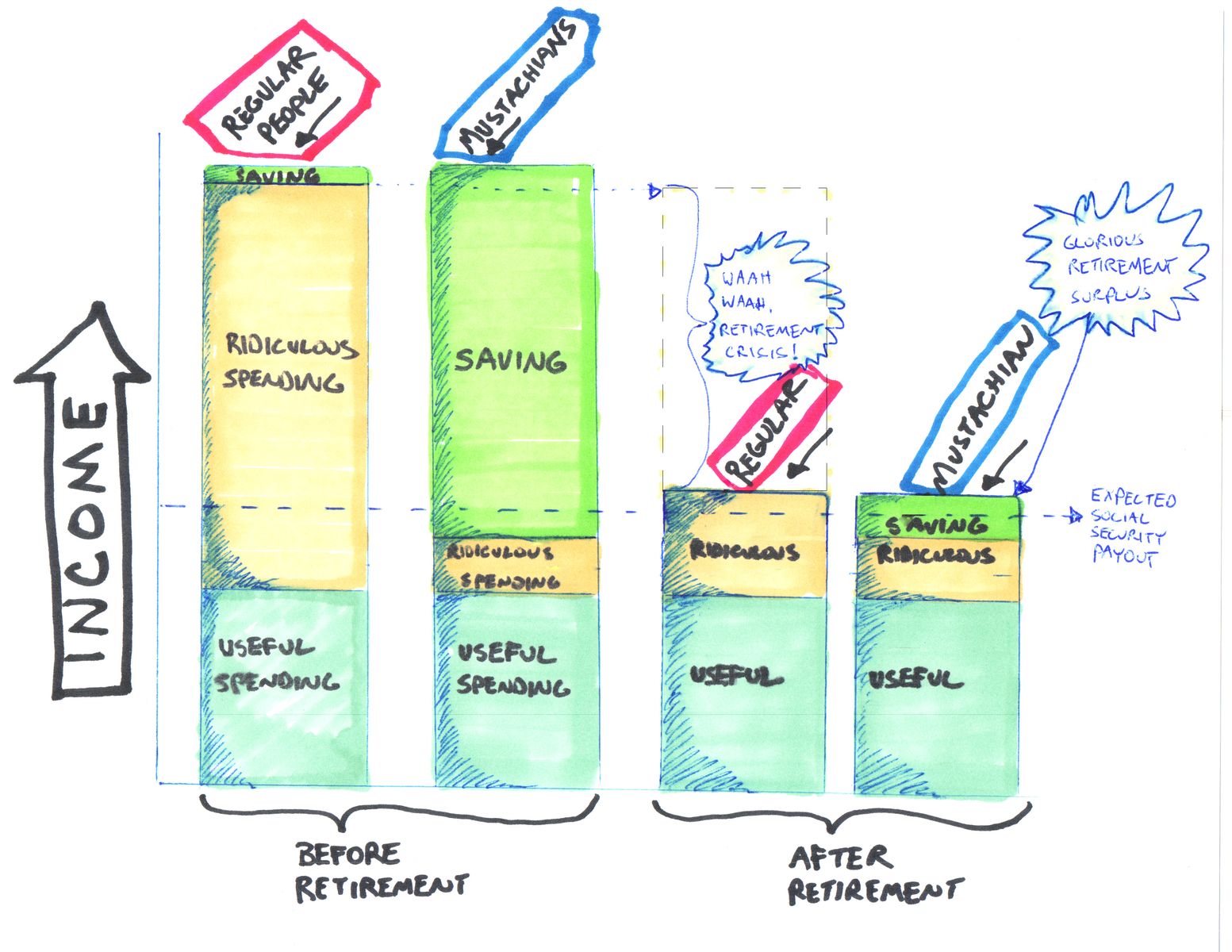

Fig.1: America's "Retirement Crisis", Illustrated with Pen and Marker

No matter how much cash you pump into a sick culture like our own, you won't solve our money problems. Because the problem is not a shortage of money - it's a shortage of spirit. A lack of desire and fire in our bellies to embrace hardship and challenge, to get the most out of ourselves, rather than designing a lifestyle that allows us to exert ourselves the least.

So that is why I take this particular stand. I know from first-hand experience, picked up on my own unremarkable journey from minimum wage to early retirement, that taking control of your own time and effort and spending is everything. The same critic that called me a "savings scold" above admits that he hasn't even started his first investment account. While there is a place for public policy in every great society, it seems unwise for those who have not yet mastered a field of study themselves, to make nationwide prescriptions on that very same field.

So let's go with a hybrid approach in solving our retirement issue. Policymakers can make sure that the Social Security program survives, because not everyone is going to become a Mustachian, and we're wealthy enough as a society that there is no need to handle people the death sentence just for poor financial skills. And sure, we should also cut down the worst thieves in the game - there is no honor in a rich person assembling a team of lawyers and marketing gurus to get poor people to sign up for a loan on a 92"^3 television.

But when it comes to talking and writing about personal finance to each other, let's drop the sympathy game. We are in control of things, not our government masters or "the elites***". We get to decide when or if to start our families, and where to settle. Our education and vocation is another choice, as is who we spend time with and how hard we work. So let us never talk about these things as if they get handed down to us from the outside world, because people are all too prone to believe it.

But most importantly of all, let's stop talking about expenses and spending as if they're out of our control and as if more is better. Even retiring with zero assets and Social Security alone is enough for a plentiful lifestyle (typically over $1500 per person per month) if you embrace the idea rather than fearing it. Living on a low wage (even minimum wage) and saving a good portion of our income is equally possible. Since there's a good chance you earn more than minimum wage, plus will have retirement savings greater than zero, there is really nothing to worry about. So, with our new freedom from worrying about stuff, let's return to work and actually get something done.

-

* OK, Mrs. Money Mustache is 50% derived from the country of India, so she only had half as much White Privilege. But that's still better than nothing. Plus there's Indian Privilege to account for as well - is that higher or lower than White? We need to factor this in to the amount of sympathy we demand.

Sure, privilege does exist, and it might make it easier or harder to inherit a company or win a senate seat. But it can't control your choice to ride a bike, buy less shit, or read library books in your spare time and I argue that frugality is the most powerful factor in earning your independence. After all, most of my equally-privileged engineering coworkers are still stuck in the office to this day.

** Isn't it funny how these doomer articles keep repeating those words even when it's not true? The recession ended in 2010 and the country returned to setting all-time records within that same year. We've been breaking new ones ever since, and the unemployment rate at 5.2% is almost as low as you can get.

*** Actually, it is possible that some of the whinier reporters might now consider Mr. Money Mustache one of "the elites". At what level do you lose your respectable credibility as a fellow underdog and become an out-of-touch elite. Do you need $100 million, $1 billion, or is simply having your mortgage paid off enough to put you out of touch with the common man's plight?

Related Reading: Top 4 SUVs for Growing Families