What to Do About These High Interest Rates

Whoa, have you seen what just happened to interest rates!?

Suddenly, after at least fourteen years of our financial world being mostly the same, somebody flipped over the table and now things are quite different.

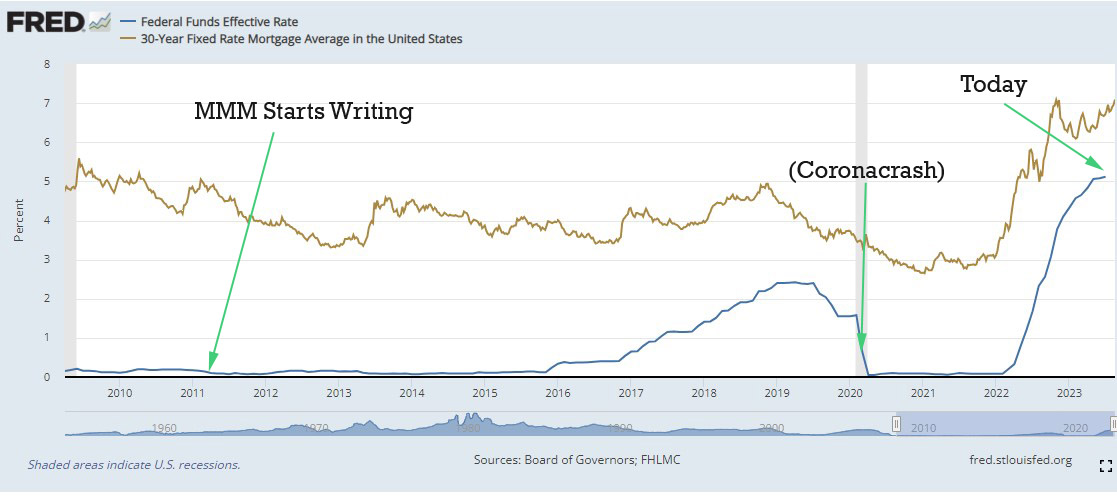

Interest rates, which have been gliding along at close to zero since before the Dawn of Mustachianism in 2011, have suddenly shot back up to 20-year highs.

-

Which brings up a few questions about whether we need to worry, or do anything about this new development.

- Is the stock market (index funds, of course) still the right place for my money?

- What if I want to buy a house?

- What about my current house - should I hang onto it forever because of the solid-gold 3% mortgage I have locked in for the next 30 years?

- Will interest rates keep going up?

- And will they ever go back down?

These questions are on everybody's mind these days, and I've been ruminating on them myself. But while I've seen a lot of play-by-play stories about each little interest rate increase in the financial newspapers, none of them seem to get into the important part, which is,

Yeah, interest rates are way up, but what should I do about it?"

So let's talk about strategy.

Why Is This Happening, and What Got Us Here?

*

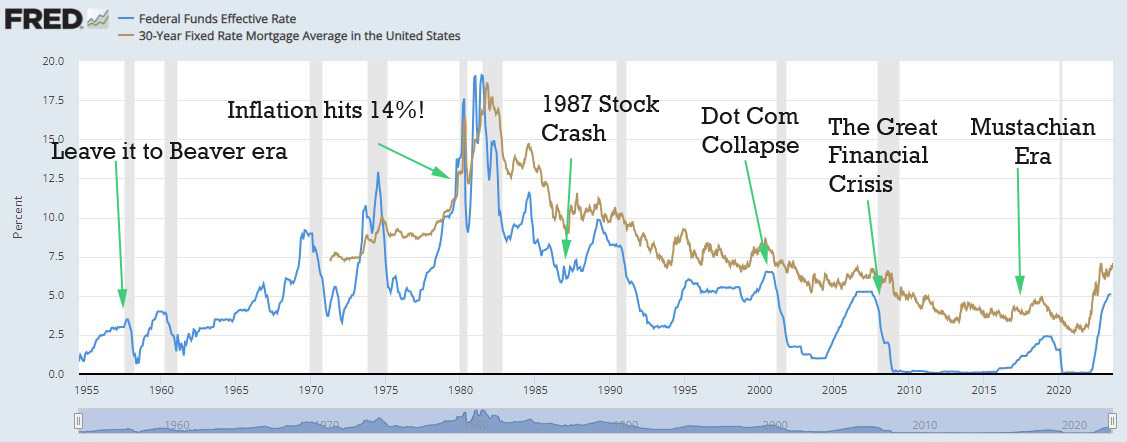

*Interest rates are like a giant gas pedal that revs the engine of our economy, with the polished black dress shoe of Federal Reserve Chairman Jerome Powell pressed upon it.

For most of the past two decades, Jerome's team and their predecessors have kept the pedal to the metal, firing a highly combustible stream of easy money into the system in the form of near-zero rates. This made mortgages more affordable, so everyone stretched to buy houses, which drove demand for existing homes and new construction alike.

It also had a similar effect on business investment: borrowed money and venture capital was cheap, so lots of entrepreneurs borrowed lots of money and started new companies. These companies then rented offices and built factories and hired employees - who circled back to buy more houses, cars, fridges, iPhones, and all the other luxurious amenities of modern life.

This was a great party and it led to lots of good things, because we had two decades of prosperity, growth, raising our children, inventing new things and all the other good stuff that happens in a successful rich country economy.

Until it went too far and we ended up with too much money chasing too few goods - especially houses. That led to a trend of unacceptably fast Inflation, which we already covered in a recent article.

Housing market distortion

Housing market distortionSo eventually, Jay-P noticed this and eased his foot back off of the Easy Money Gas Pedal. And of course when interest rates get jacked up, almost everything else in the economy slows down.

And that's what is happening right now: mortgages are suddenly way more expensive, so people are putting off their plans to buy houses. Companies find that borrowing money is costly, so they are scaling back their plans to build new factories, and cutting back on their hiring. Facebook laid off 10,000 people and Amazon shed 27,000.

We even had a miniature banking crisis where some significant mid-sized banks folded and gave the financial world fears that a much bigger set of dominoes would fall.

All of these things sound kinda bad, and if you make the mistake of checking the news, you'll see there is a big dumb battle raging as usual on every media outlet. Leftists, Right-wingers, and anarchists all have a different take on it:

- It's the President's fault for printing all that money and running up the debt! We should have Fiscal Discipline!

- No, it's the opposite! The Fed is ruining the economy with all these rate rises, we need to drop them back down because our poor middle class is suffering!

- What are you two sheeple talking about? The whole system is a bunch of corrupt cronies and we shouldn't even have a central bank. All hail the true world currency of Bitcoin!!!

The one thing all sides seem to agree on is that we are experiencing hard economic times" and that the country is headed in the wrong way".

Which, ironically, is completely wrong as well - our unemployment rate has dropped to 50-year lows and the economy is at the absolute best it has ever been, a surprise to even the most grounded economists.

The reality? We're just putting the lid back onto the ice cream carton until the economy can digest all the sugar it just wolfed down. This is normal, it happens every decade or two and it's no big deal.

Okay, but should I take my money out of the stock market because it's going to crash?

This answer never changes, so you'll see it every time we talk about stock investing: Holy Shit NO!!!

The stock market always goes up in the long run, although with plenty of unpredictable bumps along the way. Since you can't predict those bumps until after they happen, there is no point in trying to dance in and out of it.

But since we do have the benefit of hindsight, there are a few things that have changed slightly: From its peak at the beginning of 2022 until right now (August 2023 as I write this), the overall US market is down about 10%. Or to view it another way, it is roughly flat since June 2021, so we've seen two years with no gains aside from total dividends of about 3%.

Since the future is always the same, unknowable thing, this means I am about 10% more excited about buying my monthly slice of index funds today than I was at those peak prices.

Should I start putting money into savings accounts instead because they are paying 4.5%?

This is a slightly trickier question, because in theory we should invest in a logical, unbiased way into the thing with the highest expected return over time.

When interest rates were under 1%, this was an easy decision: stocks will always return far more than 1% over time - consider the fact that the annual dividend payments alone are 1.5%!

But there has to be some interest rate at which you'd be willing to stop buying stocks and prefer to just stash it into the stable, rewarding environment of a money market fund or long-term bonds or something else similar. Right now, if a reputable bank offered me, say, 12% I would probably just start loading up.

But remember that the stock market is also currently running a 10% off sale. When the market eventually reawakens and starts setting new highs (which it will someday), any shares I buy right now will be worth 10% more. And then will continue going up from there. Which quickly becomes an even bigger number than 12%.

In other words, the cheaper the stocks get, the more excited we should be about buying them rather than chasing high interest rates.

As you can see, there is no easy answer here, but I have taken a middle ground:

- I'm holding onto all the stocks I already own, of course

- BUT since I currently have an outstanding margin loan balance for a house I helped to buy with several friends (yes this is #3 in the last few years!), I am paying over 6% on that balance. So I am directing all new income towards paying down that balance for now, just for peace of mind and because 6% is a reasonable guaranteed return.

- Technically, I know I would probably make a bit more if I let the balance just stay outstanding, kept putting more money into index funds, and paid the interest forever, but this feels like a nice compromise to me

What if I want to Buy a House?

-

For most of us, the biggest thing that interest rates affect is our decisions around buying and selling houses. Financing a home with a mortgage is suddenly way more expensive, any potential rental house investments are suddenly far less profitable, and keeping our old house with a locked-in 3% mortgage is suddenly far more tempting.

Consider these shocking changes just over the past two years as typical rates have gone from about 3% to 7.5%.

Assuming a buyer comes up with the average 10% down payment:

- The monthly mortgage payment on a $400k house has gone from about $1500 at the beginning of 2022 last year to roughly $2500 today. Even scarier, the interest portion of that monthly bill has more than doubled, from $900 to $2250!

- For a home buyer with a monthly mortgage budget of $2000, their old maximum house price was about $500,000. With today's interest rates however, that figure has dropped to about $325,000

- Similarly, as a landlord in 2022 you might have been willing to pay $500k for a duplex which brought in $4000 per month of gross rent. Today, you'd need to get that same property for $325,000 to have a similar net cash flow (or try to rent each unit for a $500 more per month) because the interest cost is so much higher.

- And finally, if you're already living in a $400k house with a 3% mortgage locked in, you are effectively being subsidized to the tune of $1000 per month by that good fortune. In other words, you now have a $12,000 per year disincentive to ever sell that house if you'll need to borrow money to buy a new one. And you have a potential goldmine rental property, because your carrying costs remain low while rents keep going up.

This all sounds kind of bleak, but unfortunately it's the way things are supposed to work - the tough medicine of higher interest rates is supposed to make the following things happen:

- House buyers will end up placing lower bids which fit within their budgets.

- Landlords will have to be more discerning about which properties to buy up as rentals, lowering their own bids as well.

- Meanwhile, the current still-sky-high prices of housing should continue to entice more builders to create new homes and redevelop and upgrade old buildings and underused land, because high prices mean good profits. Then they'll have to compete for a thinner supply of home buyers.

The net effect of all this is that prices should stop going up, and ideally fall back down in many areas.

When Will House Prices Go Back Down?

This is a tricky one because the real value" of a house depends entirely on supply and demand. The right price is whatever somebody is willing to pay for it. However, there are a few fundamentals which influence this price over the long run because they determine the supply of housing.

- The actual cost of building a house (materials plus labor), which tends to just stay pretty flat - it might not even keep up with inflation.

- The value of the underlying land, which should also follow inflation on average, although with hot and cold spots depending on which cities are popular at the time.

- The amount of bullshit which residents and their city councils impose upon house builders, preventing them from producing the new housing that people want to buy.

NIMBYS in my own area, damaging the housing market.

NIMBYS in my own area, damaging the housing market.The first item (construction cost) is pretty interesting because it is subject to the magic of technological progress. Just as TVs and computers get cheaper over time, house components get cheaper too as things like computerized manufacturing and global trade make us more efficient.

I remember paying $600 for a fancy-at-the-time undermount sink and $400 for a faucet for my first kitchen remodel in the year 2001. Today, you can get a nicer sink on Amazon for about $250 and the faucet is a flat hundred. Similarly, nailguns and cordless tools and easy-to-install PEX plumbing make the process of building faster and easier than ever.

On the other hand, the last item (bullshit restrictions) has been very inflationary in recent times. I've noticed that every year another layer of red tape and complicated codes and onerous zoning and approval processes gets layered into the local book of rules, and as a result I just gave up on building new houses because it wasn't worth the hassle. Other builders with more patience will continue to plow through the murk, but they will have less competition, fewer permits will be granted, and thus the shortage of housing will continue to grow, which raises prices on average.

Thankfully, every city is different and some have chosen to make it easier to build new houses rather than more difficult. Even better, places like Tempe Arizona are allowing good housing to be built around people rather than cars, which is even more affordable to construct.

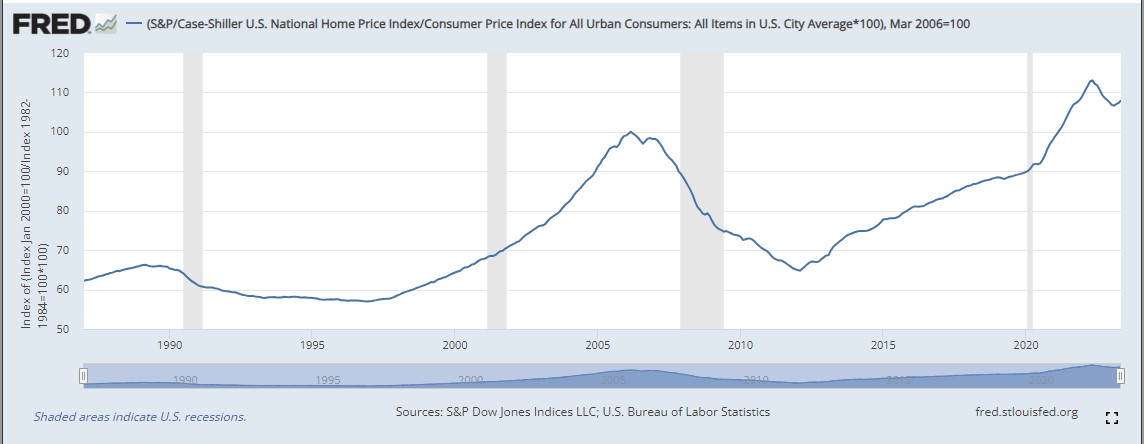

But overall, since overall US house prices adjusted for inflation are just about at an all-time high, I think there's a chance that they might ease back down another 25% (to 2020 levels). But who knows: my guess could prove totally wrong, or the fall" could just come in the form of flat prices for a decade that don't keep up with inflation, meaning that they just feel 25% cheaper relative to our higher future salaries.

Inflation-adjusted house prices over the last 35 years.

Inflation-adjusted house prices over the last 35 years.When Will Interest Rates Go Back Down?

The funny part about our current high" interest rates is that they are not actually high at all. They're right around average.So they might not go down at all for a long time.

Remember that graph at the beginning of this article? I deliberately cropped it to show only the years since 2009 - the long recent period of low interest rates. But if you zoom out to cover the last seventy years instead, you can see that we're still in a very normal range.

-

But a better answer is this one: Interest rates will go down whenever Jerome Powell or one of his successors determines that our economy is slowing down too much and needs another hit from the gas pedal. In other words, whenever we start to slip into a genuine recession.

In order to do that however, we need to see low inflation, growing unemployment, and other signs of an economy that is finally cooling down. And right now, those things keep not showing up in the weekly economic data.

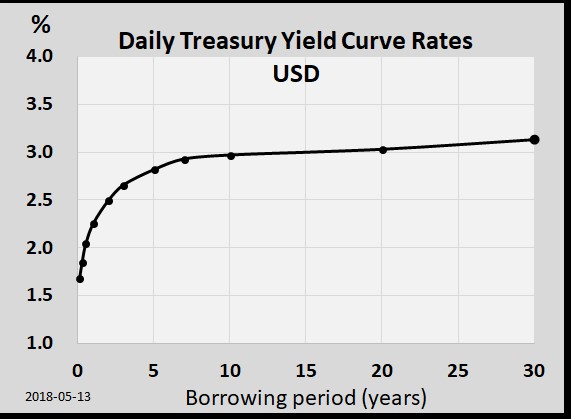

You can get one reasonable prediction of the future of interest rates by looking at something called the US Treasury Yield Curve. It typically looks like this:

-

What the graph is telling you is that as a lender you get a bigger reward in exchange for locking up your money for a longer time period. And way back in 2018, the people who make these loans expected that interest rates would average about 3.0 percent over the next 30 years.

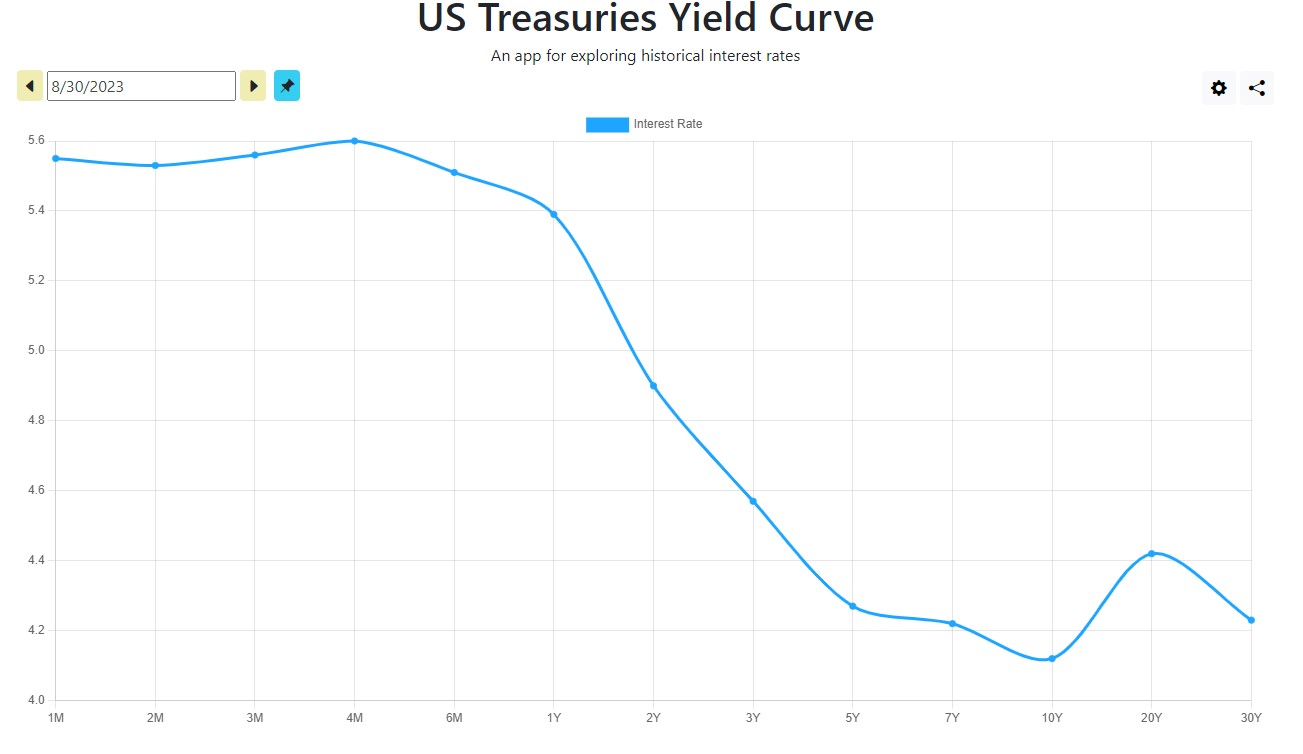

Today, we have a very strange opposite yield curve:

-

If you want to lend money for a year or less, you'll be rewarded with a juicy 5.4 percent interest rate. But for two years, the rate drops to 4.92%. And then ten-year bond pays only 4.05 percent.

This situation is weird, and it's called an inverted yield curve. And what it means is that the buyers of bonds currently believe that interest rates will almost certainly drop in the future - starting a little over a year from now.

And if you recall our earlier discussion about why interest rates drop, this means that investors are forecasting an economic slowdown in the fairly near future. And their intuition in this department has been pretty good: an inverted yield curve like this has only happened 11 times in the past 75 years, and in ten of those cases it accurately predicted a recession.

So the short answer is: nobody really knows, but just for fun I'll make a guess. Then if I'm wrong in public, you can come back and make fun of this in the comments.

I think we'll probably see interest rates start to drop within 18-24 months, and the event may be accompanied by some sort of recession as well.

The Ultimate Interest Rate Strategy Hack

-

I like to read and write about all this stuff because I'm still a finance nerd at heart. But when it comes down to it, interest rates don't really affect long-retired people like many of us MMM readers, because we are mostly done with borrowing. I like the simplicity of owning just one house and one car, mortgage-free.

With the current overheated housing market here in Colorado, I'm not tempted to even look at other properties, but someday that may change. And the great thing about having actual savings rather than just a high income that lets you qualify for a loan, is that you can be ready to pounce on a good deal on short notice.

Maybe the entire housing market will go on sale as we saw in the early 2010s, or perhaps just one perfect property in the mountains will come up at the right time. The point is that when you have enough cash to buy the thing you want, the interest rates that other people are charging don't matter. It's a nice position of strength instead of stress. And you can still decide to take out a mortgage if you do find the rates are worthwhile for your own goals.

So to tie a bow on this whole lesson: keep your lifestyle lean and happy and don't lose too much sweat over today's interest rates or house prices. They will probably both come down over time, but those things aren't in your control. Much more important are your own choices about earning, saving, healthy living and where you choose to live.

With these big sails of your life properly in place and pulling you ahead, the smaller issues of interest rates and whatever else they write about in the financial news will gradually shrink down to become just ripples on the surface of the lake.

In the comments: what have you been thinking about interest rates recently? Have they changed your decisions, increased, or perhaps even decreased your stress levels around money and housing?

-

* Photo credit: Mr. Money Mustache, and Rustoleum Ultra Cover semi gloss black spraypaint. I originally polled some local friends to see if anyone owned dress shoes and a suit so I could get this picture, with no luck. So I painted up my old semi-dressy shoes and found some clean-ish black socks and pants and vacuumed out my car a bit before taking this picture. I'm kinda proud of the results and it saved me from hiring Jerome Powell himself for the shoot.