Continued rapid growth of the global middle class could add 2.2 billion people by 2030

by noreply@blogger.com (brian wang) from NextBigFuture.com on (#2FGVZ)

Today, the global middle class, numbering about 3.2 billion in 2016, may be considerably larger - by about 500 million people than in 2010. Within a few years over half of the world's population could have middle-class or rich lifestyles for the first time ever. The most dynamic segment of the global middle-class market is at the lower end of the scale, among new entrants with comparatively low per capita spending. Homi Kharas of the Brookings Institute has provided a detailed analysis.

Over the past seven years, four relevant developments have shaped middle-class calculations, and the first two of these have quantitatively important implications for overall estimates of trends and levels.

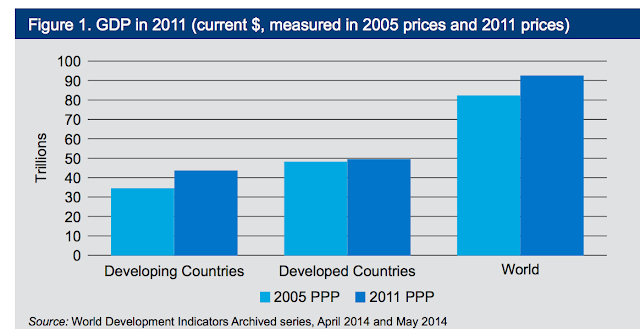

1. a survey of purchasing power parity (PPP) prices, conducted in 2011, has replaced the previous 2005 PPP survey (World Bank, 2015) as the basis for comparing real income levels across countries. The 2011 survey differs not just in updating price levels, but also uses a new methodology for generating country-level data.

The results have markedly changed and improved our understanding of countries' and households' relative economic strength. In brief, Asian and African countries were estimated to be far richer, compared to other countries, than previously imagined.

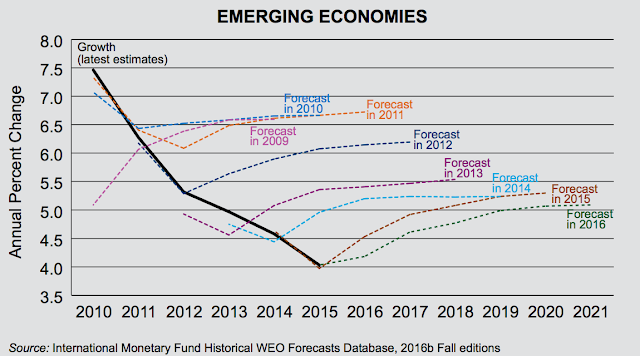

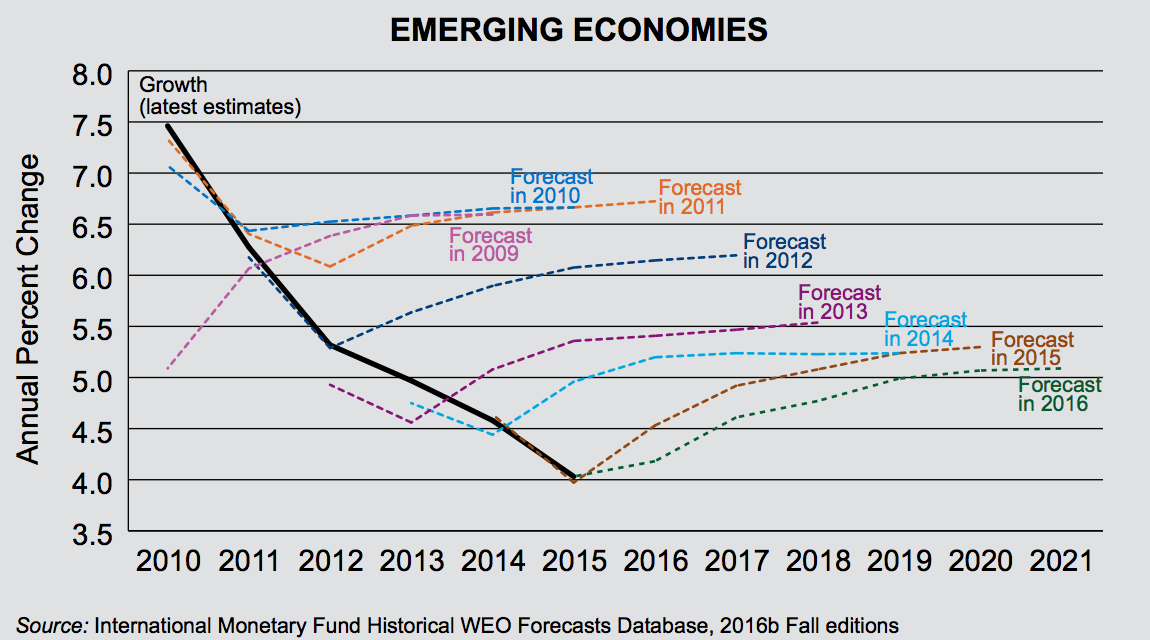

2. The continued weakness in global economic growth. Global recovery has disappointed, remaining weaker than the recovery from previous recessions (although perhaps in line with the rate of recovery from previous financial crises).

3. GDP data have improved. In some countries, (Nigeria is a good example) a rebasing of national accounts led to significant revisions of estimated output and national income.

4. several new household surveys now make it possible to undertake a more up-to-date assessment of income distribution at a time of significant changes in within-country inequality, and, in some cases, allow for direct measurement of the middle class for the first time.

The rate of increase of the middle class, in absolute numbers, is approaching its all-time peak. Already, about 140 million are joining the middle class annually and this number could rise to 170 million in five years' time.

An overwhelming majority of new entrants into the middle class- 88 percent of the next billion-will live in Asia.

The absolute market size of middle-class spending is larger than previously estimated. In 2015, middle-class spending was about $35 trillion (in 2011 PPP terms), roughly 12 percent higher than my previous estimate. It now accounts for one-third of the global economy.

Big geographic distributional shifts in markets are happening, with China and India accounting for an ever-greater market share, while the European and North American middle class basically stagnates.

At a growth of about 4 percent in real terms, the middle-class market is growing faster than global GDP growth, but not as fast as it did in the 1960s and 1970s, the boom years for the middle class.

A larger middle-class population and market has significant environment and social implications. Naturally, assuming technology does not change, the carbon footprint per person will rise as the middle class expands.

Two mitigating factors could limit the extent of this. First, middle-class growth is associated with migration from rural to urban areas and, for a given level of income, households in urban areas tend to have a smaller carbon footprint than households in rural areas, especially for transport. Second, middle-class households tend to invest more in their children's education and this, in turn, can reduce fertility rates and decrease the longterm population trajectory for the world.

The middle class has been defined by myself and many others, before and since, as comprising those households with per capita incomes between $10 and $100 per person per day (pppd) in 2005 PPP terms (Kharas, 2010; World Bank, 2007; Ernst and Young, 2013; Bank of America Merrill Lynch, 2016).

This implies an annual income for a four-person middle-class household of $14,600 to $146,000.

Taking into account inflation, the income range for middle-class families can now be expressed as $11 to $110 pppd in 2011 PPP terms.

Recently, a number of developing countries have rebased their GDP growth to account for the fact that the old GDP data may not adequately reflect the changing structural composition of GDP. Nigeria was one country that received considerable publicity. Nigeria's rebasing in 2014 lifted its GDP from $270 billion to $510 billion, becoming, in the process, the largest economy in Africa. Other countries also have rebased their GDP, with double-digit increases in several instances.

Read more

Over the past seven years, four relevant developments have shaped middle-class calculations, and the first two of these have quantitatively important implications for overall estimates of trends and levels.

1. a survey of purchasing power parity (PPP) prices, conducted in 2011, has replaced the previous 2005 PPP survey (World Bank, 2015) as the basis for comparing real income levels across countries. The 2011 survey differs not just in updating price levels, but also uses a new methodology for generating country-level data.

The results have markedly changed and improved our understanding of countries' and households' relative economic strength. In brief, Asian and African countries were estimated to be far richer, compared to other countries, than previously imagined.

2. The continued weakness in global economic growth. Global recovery has disappointed, remaining weaker than the recovery from previous recessions (although perhaps in line with the rate of recovery from previous financial crises).

3. GDP data have improved. In some countries, (Nigeria is a good example) a rebasing of national accounts led to significant revisions of estimated output and national income.

4. several new household surveys now make it possible to undertake a more up-to-date assessment of income distribution at a time of significant changes in within-country inequality, and, in some cases, allow for direct measurement of the middle class for the first time.

The rate of increase of the middle class, in absolute numbers, is approaching its all-time peak. Already, about 140 million are joining the middle class annually and this number could rise to 170 million in five years' time.

An overwhelming majority of new entrants into the middle class- 88 percent of the next billion-will live in Asia.

The absolute market size of middle-class spending is larger than previously estimated. In 2015, middle-class spending was about $35 trillion (in 2011 PPP terms), roughly 12 percent higher than my previous estimate. It now accounts for one-third of the global economy.

Big geographic distributional shifts in markets are happening, with China and India accounting for an ever-greater market share, while the European and North American middle class basically stagnates.

At a growth of about 4 percent in real terms, the middle-class market is growing faster than global GDP growth, but not as fast as it did in the 1960s and 1970s, the boom years for the middle class.

A larger middle-class population and market has significant environment and social implications. Naturally, assuming technology does not change, the carbon footprint per person will rise as the middle class expands.

Two mitigating factors could limit the extent of this. First, middle-class growth is associated with migration from rural to urban areas and, for a given level of income, households in urban areas tend to have a smaller carbon footprint than households in rural areas, especially for transport. Second, middle-class households tend to invest more in their children's education and this, in turn, can reduce fertility rates and decrease the longterm population trajectory for the world.

The middle class has been defined by myself and many others, before and since, as comprising those households with per capita incomes between $10 and $100 per person per day (pppd) in 2005 PPP terms (Kharas, 2010; World Bank, 2007; Ernst and Young, 2013; Bank of America Merrill Lynch, 2016).

This implies an annual income for a four-person middle-class household of $14,600 to $146,000.

Taking into account inflation, the income range for middle-class families can now be expressed as $11 to $110 pppd in 2011 PPP terms.

Recently, a number of developing countries have rebased their GDP growth to account for the fact that the old GDP data may not adequately reflect the changing structural composition of GDP. Nigeria was one country that received considerable publicity. Nigeria's rebasing in 2014 lifted its GDP from $270 billion to $510 billion, becoming, in the process, the largest economy in Africa. Other countries also have rebased their GDP, with double-digit increases in several instances.

Read more