|

by Katie Allen on (#10NTY)

Monetary policy committee votes to retain record low rate of 0.5% amid global uncertainty and brittle UK recoveryThe Bank of England has kept interest rates on hold this month, noting volatility in global markets and highlighting a sharp fall in oil prices that is likely to keep inflation low.Members of the Bank’s nine-member monetary policy committee (MPC) voted eight to one to leave rates at 0.5%, where they have been since March 2009, in a repeat of recent votes. Sticking to his recent stance, only Ian McCafferty voted for a rise to 0.75%.Related: The Guardian view on the economic and environmental impact of falling oil prices | EditorialRelated: UK trade deficit prompts alarm as exports fall Continue reading...

|

| Link | http://feeds.theguardian.com/ |

| Feed | http://feeds.theguardian.com/theguardian/business/economics/rss |

| Updated | 2026-07-26 23:15 |

|

by Larry Elliott on (#10MR2)

Global warming heads top economists’ concerns for first time but large-scale forced migration seen as most likely risk to materialiseA catastrophe caused by climate change is seen as the biggest potential threat to the global economy in 2016, according to a survey of 750 experts conducted by the World Economic Forum.The annual assessment of risks conducted by the WEF before its annual meeting in Davos on 20-23 January showed that global warming had catapulted its way to the top of the list of concerns. Continue reading...

|

|

by Rupert Neate in New York and Phillip Inman in Lond on (#10K61)

S&P 500 suffers its worst day since September as new data showing American fuel stockpiles have hit record levels saw Brent crude fall to below $30 a barrelUS stocks fell heavily on Wednesday, with the Standard & Poor’s 500 falling 2.5% to take the index below 1,900 points for the first time since September, due to growing concerns about the falling oil price, which dipped below $30 a barrel for the first time in nearly 12 years.The S&P 500, which closed at 1,890 points, suffered its worst day since September and has fallen by 10% since its November peak taking it into “correction†territory, something that has not happened since August 2014.Related: China sees 'many challenges' in 2016 as trade slumps on weak external demandRelated: The perils of China's currency devaluation Continue reading...

|

|

by Owen Jones on (#10K3B)

Under Obama, the economic recovery has bypassed almost all Americans. They won’t stay silent for ever – and Bernie Sanders could be their inspirationTo critique Barack Obama’s presidency is to be guilty of these cardinal sins: blasphemy, ingratitude and a lack of realism. What was once the nation of Jim Crow produced the first African-American president, the most liberal commander-in-chief since Richard Nixon (as Obama himself once put it). Funny, charming, with a coolness that eludes practically every other politician, he is the ultimate ambassador for US power. Could the United States possibly elect someone more progressive?Related: Why does Bernie Sanders continue to avoid a foreign policy platform? | Lucia GravesRelated: Bernie Sanders: free public college tuition is the 'right thing to do' Continue reading...

|

|

by Larry Elliott on (#10K2S)

Study by World Bank praises potential of technology to transform lives, but warns of risk of creating a ‘new underclass’ of the disconnectedThe rapid spread of the internet and mobile phones around the globe has failed to deliver the expected boost to jobs and growth, the World Bank has revealed in a report that highlights a growing digital divide between rich and poor.The Bank said no other technology has reached more people in so short a time as the internet, but warned that the development potential of technological change had yet to be reaped. Continue reading...

|

|

by Editorial on (#10JZZ)

Some rue the get-rich-quick allure of oil in emerging nations. Whatever happens, the geopolitical consequences of falling prices are myriad and unpredictableIn the geopolitics of oil production, predictions are always risky. However important it may be, the price of crude is never the single factor driving events. That a global shakeup will occur if the spectacular tumble in prices persists is, however, a fairly safe bet. Witness how record highs and lows in oil have affected international relations and political developments over the last four decades.The oil shocks of the 1970s reshaped the global landscape and lent new significance to the Middle East. When prices collapsed in the mid-1980s, the Soviet Union’s final demise owed much to the collapse in its export revenues. Saddam Hussein’s 1990 invasion of Kuwait derived in part from an ambition to capture new lands at a time of financial stringency. In Algeria, another country dependent on oil revenues, that same price collapse – which reduced the price of crude to below $10 a barrel – contributed to an election victory for Islamists, then a coup, and then civil war. All of this makes it difficult to draw clearcut conclusions about strategic winners and losers. Of course, the liberal democracies of the west benefited from the end of the Soviet bloc, but it is hard to argue that low oil prices in the Arab and Muslim world led to much peace and stability.Related: The Guardian view on the economic and environmental impact of falling oil prices | Editorial Continue reading...

|

|

by Jill Treanor and Larry Elliott on (#10JY4)

Other attendees will include John Kerry, Justin Trudeau, Will.i.am and Loretta Lynch, as well as the archbishop of Canterbury and representatives from UberA cast of politicians, digital pioneers, activists and Hollywood glitterati will gather in the Swiss ski resort of Davos next week for the annual World Economic Forum, which will take place against mounting fears of a new global crash.While the official theme of the five-day annual event is “the fourth industrial revolution†– a topic that will focus on the looming impact of robots and artificial intelligence – the real talking point for the 2,500 participants will be whether the violent gyrations in global financial markets since the turn of the year are evidence of trouble to come. Continue reading...

|

|

by Saeed Kamali Dehghan in London and David Smith in on (#10JTP)

Reconnecting Tehran to the global economy set to have huge ramifications for the global economy, especially the oil marketThe European Union and US are expected to formally lift sanctions against Iran this weekend, dismantling an intricate network of punitive measures built up over nearly a decade and reconnecting Tehran to the global economy.

|

|

by Graeme Wearden (until 12pm) and Nick Fletcher on (#10GSD)

All the day’s financial news, as China defies pessimism by reporting a surprise rise in exports in December

|

|

by Phillip Inman Economics correspondent on (#10F22)

Royal Bank of Scotland economists say the global economy is in for a very gloomy year indeed. Here’s what five economists thinkRoyal Bank of Scotland has warned of a “cataclysmic year†for the global economy, triggered by a slowdown in China, as it urged investors to liquidate all assets apart from high-quality bonds. The Guardian asked several economists whether they agreed with the bank’s gloomy outlook.Related: Sell everything ahead of stock market crash, say RBS economistsThe message from RBS is one of panic, which I don’t think is justified by current events. I’m worried about the outlook for the global economy, but not yet panicked.Sure, the economic indicators point to things being not so good. For instance, a sharp slowdown in China is not good for the UK, the US or Europe, because it puts a drag on growth. In that sense the impact is significant. However, it is not a disaster.We do not dispute that China will have a hard landing. It is something we have been warning about since 2009 and certain about since 2012. It is heading for 2% GDP growth and possibly lower, not the published 7%.But most people, including RBS, are overestimating the impact of China on the rest of the world. It will have a negligible effect in terms of growth in the developed world. In terms of inflation, it will have profound consequences through lower commodity and oil prices. It will also harm UK and western manufactured exports as China’s goods become cheaper and ultimately force workers in industries that compete with China to accept lower wages.The start of the year has been characterised by growing fears about the global economy and an associated rise in risk aversion, despite very little in fact changing in terms of the hard economic data.All of the current concerns, from worries about China’s debt to higher US interest rates, the winding down of central bank largesse and collapsing commodity prices, have been nagging away over much of the past year. However, it seems that optimism that the global economy can weather these headwinds is finally giving way.If you look hard enough you can always find somebody telling you markets are about to crash, but they are normally wrong. Historically equities have been the best asset class over the long term – listening to the doom-mongers has been a mistake.Today’s disappointing industrial production figures suggest the [UK] economy slowed toward the end of 2015, and is still heavily reliant on consumer spending. However, growth is steady (if unspectacular), the labour market continues to show encouraging signs and interest rates look unlikely to rise any time soon.This is a scary warning from RBS but it doesn’t seem sensible to spook investors. As Keynes made clear consumer and business confidence matters – he called them animal spirits. Volatility is high but a great collapse doesn’t seem to be in the air. It doesn’t make sense to talk down markets as that can become self- fulfilling.The year started badly in stock markets around the world as China looked to be in free fall. Things look a little better now. The worry for the UK is that the government failed to fix the roof when the sun was shining over the last five years or so. Even the chancellor has pointed to a cocktail of risks in direct contrast to his position at the autumn statement in November. The concern is that the economy is at a turning point. We shall see. There are tough days ahead but there is no reason to panic. Not yet anyway. Continue reading...

|

|

by Megan Darby for Climate Home, part of the Guardian on (#10HDV)

Influential financial body estimates $30/tonne tax on emissions from international transport could have raised $25bn in 2014, reports Climate HomeThe International Monetary Fund is calling for a carbon tax on aviation and shipping to help deliver global climate goals.

|

|

by Mohamed El-Erian on (#10H1D)

In pursuing its domestic objectives, China risks inadvertently amplifying global financial instabilityThe recent decline in China’s currency, the renminbi, which has fuelled turmoil in Chinese stock markets and drove the government to suspend trading twice last week, highlights a major challenge facing the country: how to balance its domestic and international economic obligations. The approach the authorities take will have a major impact on the wellbeing of the global economy.The 2008 global financial crisis, coupled with the disappointing recovery in the advanced economies that followed, injected a new urgency into China’s efforts to shift its growth model from one based on investment and external demand to one underpinned by domestic consumption. Navigating such a structural transition without causing a sharp decline in economic growth would be difficult for any country. The challenge is even greater for a country as large and complex as China, especially given today’s environment of sluggish global growth. Continue reading...

|

|

by Jana Kasperkevic in New York on (#10FGS)

Growth in the solar industry was not shared equally across all types of jobs in 2015 – employees of installation companies accounted for 65% of jobs addedThe US solar industry now employs more workers than oil and gas, a new report from the Solar Foundation claims, with most of the jobs in power panel installation.Last year, the US solar industry grew by 20% for a third year in a row, according to the foundation’s National Solar Job Census 2015. By the end of 2015, it employed nearly 209,000 solar workers, more than those employed in oil and gas extraction.Related: Oil price forecast to fall to $20 a barrel, predicts Morgan Stanley Continue reading...

|

|

by Editorial on (#10F75)

Brussels is cracking down on tax breaks for big business. And about time tooThe sentence that follows may be among the rarest in British newspapers, but here goes. A big hand for the European commission for doing an excellent thing. This week, the commission ruled that Belgium has been granting an illegal tax break to at least 35 global companies. The Belgian government will now be forced to recover the unpaid taxes – equivalent to about £530m – from the companies. Last October, it was Luxembourg that was in the firing line – ordered by the commission to recover up to £22.5m from a subsidiary of Fiat. The Netherlands also ran into grief last year over a deal it made with Starbucks. All three countries have been caught out by a series of investigations led by the EU’s competition commissioner, Margrethe Vestager, into countries cutting special tax deals with massive multinationals. The EU is going after cases where member countries have granted individual tax breaks to big companies, without making them available to all the businesses there.How much money is at stake? Consider Anheuser-Busch InBev, the largest brewer in the world, the manufacturer of Stella Artois and Budweiser among others, and capitalised on the stock market at $189bn. It has a Belgian subsidiary making profits of about £45m a year. Belgium’s official corporate tax rate is 34%, which implies that the unit should pay about £15m a year in corporation tax. Instead it enjoys a rate of about 4% which brings its corporation tax payments down closer to £1.8m a year. Its parent company also has its headquarters in Belgium and, according to the New York Times, paid “a small fraction of 1% on its reported profit of … $1.93bn [£1.34bn] in 2014â€. Continue reading...

|

|

by Larry Elliott, Economics editor on (#10F38)

Albert Edwards joins RBS in warning of a new crash, saying oil price plunge and deflation from emerging markets will overwhelm central banks, tip the markets and collapse the eurozoneThe City of London’s most vocal “bear†has warned that the world is heading for a financial crisis as severe as the crash of 2008-09 that could prompt the collapse of the eurozone.

|

|

by Graeme Wearden (until 3.35) and Nick Fletcher on (#10D3Q)

IMF chief says global economy needs to tame hot money, to help developing economies achieve stable growth

|

|

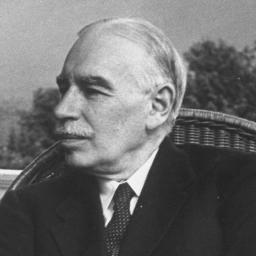

by Larry Elliott Economics editor on (#10E4P)

Study of Keynes’s foreign exchange dealings between the first and second world wars reveals a chequered recordMarkets can remain irrational longer than you can remain solvent. Such is the advice John Maynard Keynes is supposed to have given to would-be investors looking to make a killing in the period between the first and second world wars.There is some dispute about whether Keynes ever delivered this warning. What is not at issue is that it was advice he did not always follow, especially when it came to his dabblings in the currency market. Continue reading...

|

|

by Larry Elliott on (#10DWV)

Five years on from pledge to rebalance the economy, manufacturing output is no higher than in 2011, with sector officially back in recessionA Britain “carried aloft by the march of the makersâ€. That was the country George Osborne envisaged in the peroration to his 2011 budget speech. The message from the chancellor was clear; gone were the days when the economy relied on debt-fuelled spending. The clock was being turned back to the days when Britain actually made stuff.Related: Weak UK manufacturing data hits the pound - business liveRelated: UK's industrial sector ends 2015 on a low note Continue reading...

|

|

by Jonathan Watts in Rio de Janeiro on (#10DJY)

Austerity does not come naturally to Brazilians, but attitudes are changing as economy suffers what is forecast to be the deepest crisis in more than a centuryWhen it comes to mood making in Brazil, there are few institutions that can match the samba schools of Rio de Janeiro.

|

|

by Phillip Inman Economics correspondent on (#10DJ6)

Output declined in November, amid Chinese woes and a falling oil price, setting the tone for a difficult 2016The pound has tumbled to its lowest against the dollar since June 2010 as investors reacted to an unexpected and broad-based downturn in Britain’s industrial sector that hit factory output, mining and energy production.Related: Weak UK manufacturing data hits the pound - business liveRelated: March of the makers remains a figment of Osborne's imagination Continue reading...

|

|

by Martin Farrer and agencies on (#10CQF)

Despite fighting words from the central bank and Communist party leaders, banks are calling the currency lower, pulling oil and stocks down furtherThe Chinese authorities have resorted to “nuclear strength†weapons to deter an attack on the yuan by short sellers and convince sceptical investors that they are in control of the country’s spluttering financial system.

|

|

by Shalailah Medhora on (#10CM3)

Government continues to trumpet Trans-Pacific Partnership’s ‘enormous benefits’ despite analysis showing Australia’s growth will be worse than 11 of the other 12 countries in the dealThe federal government maintains the Trans-Pacific Partnership agreement will deliver “enormous benefitsâ€, despite World Bank analysis showing Australia’s economy will grow by less than 1% as a result of the deal.Australia’s increased growth is projected to be worse than 11 of the other 12 countries that signed the deal last year, according to the report on the global implications of the deal. Only the US fares worse. Continue reading...

|

|

by Larry Elliott on (#10BE0)

Leading Wall Street bank says price will keep falling if China’s currency continues its plunge against US dollarThe price of crude oil could tumble to $20 a barrel in the coming months if China’s currency continues to decline against the US dollar, one of Wall Street’s leading investment banks has predicted.On a day when the cost of crude hit a new 12-year low and edge closer to the $30 a barrel level, Morgan Stanley posted a forecast on Monday of $20-25 a barrel for oil based on movements in currencies.Related: China shares fall another 5%, Europe slips back as oil tumbles - as it happened Continue reading...

|

|

by Graeme Wearden (unitl 2.45) and Nick Fletcher on (#109M1)

All the latest economic and financial news, as Shanghai stocks slide again despite Beijing’s claims that its financial system is ‘largely stable and healthy’

|

|

by Paul Mason on (#10BAX)

If its first week is anything to go by, 2016 could be an even more turbulent year than the last. Is there an antidote to barbarity and economic decline?As the world’s attention was captured by Madaya, the Syrian town suffering mass starvation, supporters of the Assad regime began posting photographs of delicious food to insult those starving. When a Muslim woman stood in silence at Donald Trump rally, wearing a T-shirt saying “I come in peaceâ€, she was ejected – Trump’s supporters baying insults into her face.Meanwhile, groups of apparently foreign men in Cologne staged what look like premeditated sexual assaults on women, prompting a new outburst of the racism barely hidden behind German constitutional reality.Related: High demand for reprint of Hitler's Mein Kampf takes publisher by surprise Continue reading...

|

|

by Staff and agencies on (#1093K)

Monday’s fall in share prices followed a 10% plunge last week which triggered a global sell-off of riskier assetsChinese shares fell 5% to a three-month low after confusion about the direction of the Chinese currency caused wild gyrations on Asian stock markets.A late rush of selling in Shanghai sent the CSI 300 index down 169 points to 3,192 points – its lowest since the aftermath of the summer crisis.Related: Stock market turmoil: China shares fall another 5% - business liveRelated: Australia bet the house on never-ending Chinese growth. It might not end well Continue reading...

|

|

by Greg Jericho on (#1090H)

Enjoy that refreshed feeling while it lasts – analysts warn that China is in a huge credit bubble, and the jitters can’t be far away for Australian investorsIt’s always great to come back from the holidays ready to get into the new year afresh. Alas, the early signs this year on the economic front are hardly fresh – indeed they seem gloomily repetitive of last year.Related: Australia bet the house on never-ending Chinese growth. It might not end wellRelated: Slowing growth in China raises red flag for global economyRelated: A volatile world is sending stock markets tumbling but don't panicRelated: China interest rate cut fuels fears over ailing economy Continue reading...

|

|

by Phillip Inman Economics correspondent on (#108VP)

Business trends report pinpoints growing job prospects, price cuts and low interest rates

|

by Lindsay David on (#1089G)

Assumptions about coal and iron ore exports helped build Australian prosperity. But with China’s economy threatening to unravel, a less rosy picture is emergingOver the last couple of decades, China has undergone profound change and is often cited as an economic growth miracle. Day by day, however, the evidence becomes increasingly clear the probability of a severe economic and financial downturn in China is on the cards. This is not good news at all for Australia. The country is heavily exposed, as China comprises Australia’s top export market, at 33%, more than double the second (Japan at 15%).Related: Is 2016 the year when the world tumbles back into economic crisis?Related: Deja vu for Australian economy as China woes portend another bad year Continue reading...

|

by Larry Elliott Economics editor on (#10834)

Donor countries are increasingly dipping into their aid budgets to deal with the migration crisisSweden is one of the most generous countries in the world when it comes to international aid. Along with other Scandinavian countries, it has given bounteously to less fortunate nations for many years. With a population of under 10 million, it also takes more than its fair share of asylum seekers - an estimated 190,000 last year, with a further 100,000 to 170,000 expected to arrive in 2016.

|

|

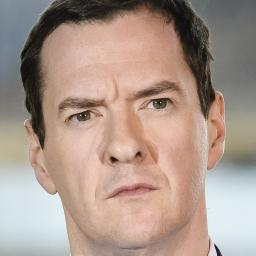

by William Keegan on (#106TP)

George Osborne is now warning of ‘dangerous complacency’ just months after his notably complacent performance in the autumn statementDangerous cocktails were in evidence in many a bar during the Christmas and New Year holidays. I do not know how many the chancellor might have sampled, but his demeanour appears to have been transformed from one of blatant complacency in his autumn statement to pre-budget nerves. He now warns of “a dangerous cocktail of new threats†and, yes, “creeping complacency†in the British economic and political debate.This is not, of course, anything to do with him and the complacency he was fostering as recently as before Christmas. No, this is mainly because of threats to the global economic recovery emanating from a manifest slowdown in China and the impact the collapse of oil prices is having on the economies and finances of oil-producing nations – with the obvious exception of the oil-producing country known as the United States, whose “fracking†boom has made no small contribution to oversupply and falling prices in energy markets. Continue reading...

|

|

by Josh Bivens on (#106CF)

The economic fundamentals will remain perilous if low- and middle-income workers continue to endure poor payThe US economy ended 2015 with improvement in the labour market. Jobs grew by 284,000 each month on average in the last quarter and if you squint pretty hard at the data you can see a mild acceleration in the pace of nominal wage growth.There will be plenty who will claim this justifies the Federal Reserve’s decisions to raise short-term interest rates for the first time since 2007, and who will argue further that the economic concerns raised by the great recession and its aftermath can now be reshelved. They would then conclude that the focus can return to policy perennials like the need to reduce deficits and ensure that wage and price inflation do not spiral out of control. Continue reading...

|

|

by Larry Elliott on (#10573)

Some see China’s share collapse as merely a symptom of middle-class prosperity. Others take a darker view – and if they are right, the global threat is realRarely have financial markets had a more traumatic start to the year. Shares plunged, the price of oil clattered to its lowest level in 11 years, trading on the Chinese stock market was halted twice, and the World Bank warned that a “perfect storm†might be brewing.George Osborne chose his moment well to go public with his concern that the UK faces a “cocktail of threatsâ€. In addition to the $2tn wiped off global stock markets, the North Koreans claimed they had exploded a hydrogen bomb and relations between Saudi Arabia and Iran worsened markedly. Continue reading...

|

|

by Katie Allen and Tom Phillips in Beijing on (#102P1)

Anxiety grips markets as sharp drops on world’s biggest stock exchanges mirror tumbling shares in BeijingA punishing week has left global stock markets nursing losses of more than $2tn in the first week of the new year after worries about China’s faltering growth and turmoil on its stock exchanges reverberated around the world.Almost £85bn was wiped off the FTSE 100 in its worst opening week to a year since 2000, when the dotcom bubble burst. The blue-chip index closed at 5,912.44 on Friday, down 0.7% on the day and 5.3% on the week. Continue reading...

|

|

by Letters on (#102JD)

So George Osborne tells us we face a “dangerous cocktail†of global risks to the economy (Report, 7 January). The Middle East, China, oil prices, US interest rates, terrorism … But I remember he told us that it was just Gordon Brown.

|

|

by Martin Farrer in Sydney, Graeme Wearden and Nick F on (#ZZXD)

Investors have been buoyed by the People’s Bank of China’s decision to boost the yuan for the first time in nine days. US jobs showed stronger than expected growth, prompting rate hike talk

|

|

by Owen Hatherley on (#1025T)

It is on posters, mugs, tea towels and in headlines. Harking back to a ‘blitz spirit’ and an age of public service, ‘Keep Calm and Carry On’ has become ubiquitous. How did a cosy, middle-class joke assume darker connotations?To get some sense of just what a monster it has become, try counting the number of times in a week you see some permutation of the “Keep Calm and Carry On†poster. In the last few days I’ve seen it twice as a poster advertising a pub’s New Year’s Eve party, several times in souvenir shops, in a photograph accompanying a Guardian article on the imminent doctors’ strike (“Keep Calm and Save the NHSâ€) and as the subject of too many internet memes to count. Some were related to the floods – a flagrantly opportunistic Liberal Democrat poster, with “Keep Calm and Survive Floodsâ€, and the somewhat more mordant “Keep Calm and Make a Photo of Floodsâ€. Then there were those related to Islamic State: “Keep Calm and Fight Isis†on the standard red background with the crown above; and “Keep Calm and Support Isis†on a black background, with the crown replaced by the Isis logo. Around eight years after it started to appear, it has become quite possibly the most successful meme in history. And, unlike most memes, it has been astonishingly enduring, a canvas on to which practically anything can be projected while retaining a sense of ironic reassurance. It is the ruling emblem of an era that is increasingly defined by austerity nostalgia.I can pinpoint the precise moment at which I realised that what had seemed a typically, somewhat insufferably, English phenomenon had gone completely and inescapably global. I was going into the flagship Warsaw branch of the Polish department store Empik and there, just past the revolving doors, was a collection of notebooks, mouse pads, diaries and the like, featuring a familiar English sans serif font, white on red, topped with the crown, in English:Few images of the last decade are quite so riddled with ideology, and few ‘historical’ artefacts are so utterly falseRelated: Keep Calm and Carry On: The secret historyAt Jamie’s restaurants you can order pork scratchings for £4 and enjoy neo-Victorian toilets Continue reading...

|

|

by Larry Elliott Economics editor on (#101WW)

The creation of 300,000 jobs last month sounds great but wages and manufacturing data are just as important, and both point to weaknessIt seems just like the good old days. Almost 300,000 jobs were added to payrolls in America in the last month of 2015, continuing the upward trend of recent months. The US is once again living up to its reputation for being a gigantic jobs machine.Well, perhaps. Jobs are certainly being created at a good lick and the US has an unemployment rate – 5% – that the eurozone, at 10.5%, would die for. There are signs that people who had given up hope of finding work are being encouraged back into the labour market.Related: China closes 2% higher while US job figures beat forecasts – live Continue reading...

|

|

by Julia Kollewe in London and Tom Phillips in Beijin on (#10195)

Chinese ‘national team’ of state-owned banks buy yuan sending signal that Beijing is not seeking to devalue currencyOil prices have rebounded and global stock markets recovered after Beijing mustered what analysts called its “national team†to intervene and boost the yuan.The price of Brent crude, the global benchmark, rose more than 2% and later traded 1.8% higher at $34.36 a barrel. On Thursday, it had hit $32.16, the lowest since April 2004.Related: Chinese stock market closes 2% higher after 'national team' intervenes – live Continue reading...

|

|

by Phillip Inman Economics correspondent on (#1016F)

Analysts say narrowing trade gap from £3.5bn to £3.2bn was powered by a big drop in oil imports and UK exports are not improvingBritain’s trade gap remained alarmingly high in November after exports fell to their lowest value since July.Official figures showed the deficit in goods and services narrowed to £3.2bn compared with £3.5bn in the previous month, but this was only after a drop in oil imports and a £2.4bn fall in the value of “unspecified goodsâ€, mainly gold, brought into the country.Related: George Osborne’s ‘cocktail of threats’ will leave us with a hangover | John McDonnell Continue reading...

|

|

by John McDonnell on (#10122)

The chancellor promised 2015 would be the year government borrowing would hit zero, but we’re facing a noxious economic brew of his own makingGeorge Osborne yesterday warned us about a “cocktail of threats†brewing in the world economy. All the ingredients are there for a noxious brew. The emerging markets debt bubble. The ongoing stock market turmoil in China. Recession in Brazil and Russia, and the slowdown in India. The collapse in global commodity prices.I’ve warned about the danger signs elsewhere before. But curiously, Osborne didn’t talk up these “threats†in last year’s autumn statement. He didn’t raise them at the summer budget. They were hardly a centrepiece of his election campaign.Related: George Osborne warns UK economy faces 'cocktail of threats'I doubt even Osborne believes his own stories any more. That’s why he’s getting his excuses in firstRelated: I’m backing George Osborne’s Project Fear – if it helps keep us in Europe | Martin Kettle Continue reading...

|

|

by Katie Allen on (#100HW)

Treasury select committee chair said ONS lacked intellectual curiosity, was prone to silly mistakes and was unresponsive to consumer needsAndrew Tyrie, the chairman of the Treasury select committee, has redoubled his criticism of the Office for National Statistics (ONS) for falling behind its international peers and jeopardising policy decisions with poor quality data.

|

by Editorial on (#ZZS6)

The high street giant was built on high-volume sales to a mass market, but that business model is bustMarks & Spencer is not dying: it owns more than a thousand stores, often in prime high street sites. Last year, it made more than £600m profit. Its revenues are huge: over £10bn, which is about the equivalent of the GDP of a country the size of Malta. So there is plenty of life in it yet. But it is wounded, and trying to heal it is turning out to be much harder than even Marc Bolland, the smooth-talking Dutch chief executive expected. On Thursday, along with disappointing clothes and homeware sales figures, he announced his unexpectedly early departure.If restoring this behemoth of the retail economy to robust good health was going to be easy, it would have happened years ago. Mr Bolland is well-regarded. The company’s share price has been on an erratic but generally upward trajectory ever since he took over more than five years ago. He appears to have cracked the worst glitches in the digital sales business, and the food side continues to grow at a steady rate. But the old staples of knickers and knitwear are floundering and the search for the perfect homeware offer goes on. Retail analysts think his successor, Steve Rowe, will have an easier task than Mr Bolland did. There are plenty of reasons why he won’t. Continue reading...

by Graeme Wearden on (#ZX2A)

Markets slide around the globe after Chinese regulators are forced to halt trading for the second time this week

|

by Katie Allen and Graeme Wearden on (#ZZ10)

Decision to abandon mechanism came after it was tripped for a second time in a week when market fell 7% within minutes of openingChinese authorities sought to bring an end to new year stock market turmoil with a dramatic U-turn on a new mechanism that Beijing had hoped would prevent sharp selloffs.On Thursday, in a tacit admission that the new circuit breakers introduced only this week were having the opposite effect to that intended, China’s main stock exchanges said they were suspending the mechanism. The move came after the breaker was tripped for the second time in a week as the market fell 7% within half an hour of opening.Related: China share trading halted after market plunges 7% in opening minutes Continue reading...

|

|

by Letters on (#ZYZ4)

I see clutter (Suzanne Moore, G2, 7 January) more as a “symptom†than a “problemâ€. Clutter and consumerism are symptoms of excessively cheap products with the true price being paid somewhere else down the line in the form of exploitative labour practices, environmental degradation or excessive use of fuel. The explanation is simple: our homes are full of “tat†because all that stuff is so cheap to buy. The solution is to put an end to the perpetual shopping spree that is modern life. If we created the economic conditions (using taxation, tariffs and regulation) so that far more everyday items were manufactured closer to home, this would quickly declutter everyone’s homes because, when you pay the full cost of locally produced shirts (for example), rather than sweatshop-produced ones, you demand higher quality, you buy far fewer, you appreciate them more and you wear them longer. The result: your clutter disappears.

|

|

by Larry Elliott on (#ZYXS)

Chancellor’s ominous speech to business leaders in Cardiff suggests he knows some nasty piece of news we don’t – possibly about the budget deficitBritain faces a “dangerous cocktail†of threats. There is a culture of “creeping complacency†that the economy is problem free. The biggest risk is that people forget about the recession and assume that it is “job doneâ€.Business leaders who turned up to listen to George Osborne in Cardiff on Thursday could be forgiven for wondering what’s happened to the chancellor who delivered such an upbeat autumn statement six weeks ago.Related: Lies, damned lies, national statistics: Bean accounts for the counters Continue reading...

|

by Katie Allen on (#ZYWR)

Billionaire investor-turned-philanthropist says China’s struggle to find a new growth model is spreading problems to the rest of the worldBillionaire speculator George Soros has added to the gloom in global markets by claiming the world risks a return to the turmoil of the 2008 financial crisis.Soros, who famously helped to force the pound out of the exchange rate mechanism on Black Wednesday in 1992, highlighted China’s struggles to find a new growth model and said its currency devaluation was spreading problems to the rest of the world. Continue reading...

by Guardian Staff on (#ZYWS)

Chancellor George Osborne warns of threats faced by Britain’s economy, including stock market falls, and problems abroad with China’s market slowing and economic instability in Russia and Brazil. Despite the challenges ahead, Osborne says that 2016 is the year ‘we can get down to work and make the lasting changes Britain so badly needs’

|

by Andrew Sparrow on (#ZX9D)

Rolling coverage of all the day’s political developments as they happen

|